Strategic Planning

It is important to focus on developing a longer term strategy for your company. However, in order to develop a strategy it is vital that your company first understands your position in the market (see other resources on Market Positioning). While there are many differing views of how to develop a strategy or strategic plan for a business, the following is designed to be a shortened and workable approach. Keep in mind that a strategic plan is a living document. Therefore, the Giersch Group’s approach to the annual cycle helps, because next year’s plan will build off of this year’s plan. With this in mind we recommend a 3 year strategic plan.

Step 1: The Mission Statement

A strategy focuses the business into what it wishes to achieve and holds it back from pursuing opportunities that are inconsistent with its strategy. In order to provide focus, companies often begin by developing a vision or mission statement. This guiding statement--and the constant affirmation of it-- leads to clarity and focus of all goals and activities. Each day this vision will guide your purpose and direction as a company. While we all know that mission/vision statements are more than “making more money,” many a company suffers from just this as their real core mission. While small companies may think that each employee is aware of the vision, a written statement that is clearly communicated will ensure consistency of the vision both now and as the company expands.

Step 2: Establish a Target

The target is what the business should be in the next three years. To do establish a target we recommend answering two questions: 1) What do you see the business as in three years and 2) What would the business look like if it doubled in three years. These questions play off of each other in that most owners view the business future in an incremental growth fashion, therefore the doubling question causes an “out of the box” evaluation of the business and its opportunities. Answering these questions starts with revenue and then adds the operational actions to support the targeted revenue. Market positioning analysis is very helpful in thinking through the answers to these questions. If a competitor is going out of business, the potential for growth may be enhanced. New products may create additional opportunities. Pricing changes effect revenue and cost growth. It is important to factor in inflation in order to see real growth. For example, if the business is doing $2.5 million in 2008 and the sense is that $3 million would be a good target in 2011, most of the added revenue is just inflation. There is little real growth.[1] The doubling question will create a real challenge to our thinking. What does this business look like in 2011 doing $6 million? This means real growth. After evaluating these two questions, a target needs to be chosen. In this example, a target of $4.5 million might be chosen as realistic, giving consideration to the market position and growth dynamics needed.

Step 3: Identify Annual Steps to Achieve the Target

Now that a target has been set for what the business should look like in three years, the current state of the business is compared to that target to develop the differences or changes to be made over the next three years. The Giersch Group offers a Business Review which utilizes a SWOT (Strengths, Weaknesses, Opportunities, Threats) analysis to help the company determine their current position. This knowledge lays a nice foundation for identifying the necessary steps from today through year three to reach the target desired.

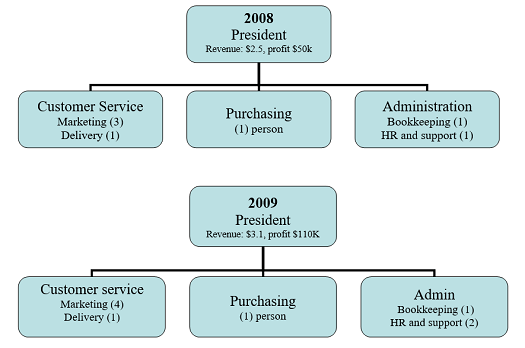

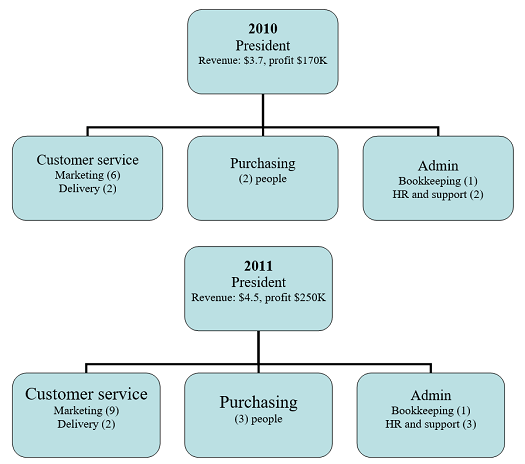

Organizational changes need to be written down and the steps to accomplish each one described briefly. One visual way that future growth can be charted is through showing the changes in an organizational chart year by year. These charts can demonstrate growth areas through staff or product/service offering additions. Without framing the necessary steps for each goal, the target is unlikely to be reached. An illustration for example is shown at the end of this article in Exhibit A. Note that it is a simple model for illustration purposes. The revenue targets could be pushed down to the marketing team as well as being at the president level.

Step 4: The Financial Model

Once the components of the strategy are identified, then a financial model for the next 3 years is critical. The model brings the strategy to life. A good model will follow the financial statement format that was discussed in the April Topic: a balance sheet, income statement and statement of cash flows. The level of detail is always a question. For a first time model, we recommend a simplified approach showing the following on the income statement.

- Revenue for the year

- A sub-schedule with customers or products to show the sourcing of the revenue is very helpful.

- Marketing or other revenue generation resources are noted here, but will be in the costs section, below.

- Cost of goods sold

- The margin questions discussed in the March topic are useful here. What is looked for is whether margins will change or can be changed over the next 3 years.

- COGS links to the balance sheet through the inventory. It is important to note whether growth in revenue will require more inventory, which means more investment. Thus the balance sheet is critical.

- Sales, General and Administration

- Are there needed marketing resources, facilities, or support for the growth?

- Operating income

- Taxes

- Taxes are always important. Even pass-through entities such as S-corps, LLCs and partnerships have to provide cash to their investors/owners to pay taxes.

- Net income

The income statement then flows through a balance sheet and cash flow statement. The key here is to identify what added investment is required to support the growth. Without added facilities, added investment may be required for Accounts Receivable, Inventories, etc, reduced by any growth in Accounts Payable. These should be developed by making sure the ending balances on these accounts are based upon the average amount for the current level of revenue. [Yes, this can be the tricky part of the model, but it is important.]

Strategy: Communication

Most staff are caught up in day-to-day activities, but are interested in knowing where the company is today and where it will be in three years. Staff support for the execution of the plan is critical. A written down plan can be communicated to the staff and then it can reviewed regularly for progress, used to evaluate opportunities, and adapted as the market changes.

Articles for Further Reading

- “Persuasive Projections.” This article discusses the necessary elements of financial projections particularly focusing on what loan officers and investors are looking for. http://www.inc.com/magazine/20000401/18118.html

- ‘Living’ Business Plans help Businesses Flow with Future. This article tells the story of a company who was able to adjust their strategic plan quickly when learning that their business was seasonal in nature. http://www.inc.com/articles/2000/03/18184.html

- “Making Your Financials Add Up.” This article focuses on developing an accurate financial forecast for revenues rather than broad guesses and general percentage increases. http://www.inc.com/articles/2002/03/24019.html

- “Strategic Planning: Not Just for Big Business.” This article addresses the difference between strategic and business plans and sets forth parameters for strategic plans for the small business owner. http://www.smallbusinessnotes.com/planning/strategicplanning.html

- “Integrated Measurement Systems.” This article explains the purpose of the balance scorecard management tool and how to create one for your company. http://www.toolpack.com/scorecard.html

- “Small Business Management Audit.” This 9 question article helps you quickly audit your firm regarding strategic planning. http://www.prenhall.com/scarbzim/html/audits/audit2.html

For more information, please visit the Giersch Group at http://www.gierschgroup.com/ or contact us at prosper@gierschgroup.com

Exhibit A: Strategic Plan Model Example

Assumptions:

- Current business does $2.5 million, has a profit of $50,000 for 2008.

- Target for 2011 is $4.5 million with a profit of $250,000

- Target is set based upon adding new customers and developing existing customer base

- Added profit is based on maintaining a 10% profit margin on the added revenue.

- Needed investment is viewed as minimal due to adequate inventories. Result will be higher inventory turns.

- Added resources for marketing and customer services will be needed to handle added activity.

- No added administration staff will be needed.

[These key assumptions are based on looking at the current situation as compared to the 2011 target.]