How to Improve the Efficiency of your Cash Flow Cycle

Master the basics of cash flow management & grow your business

Entrepreneurs know that “cash is king” in every business. Therefore, managing cash flow is a vital consideration for any small business. Understanding the demand on your company’s cash can allow you to make wise investments and secure your company’s growth. Key questions a small business should answer: What is our current cash position? Do we have enough cash to pay for our expenses? Is our cash cycle efficient? And what should we do with excess cash? To manage your company’s growth, you must do four things:

- Know your current cash position

- Anticipate cash needs

- Improve efficiency in cash flow

- Invest extra funds wisely

Get a free cash flow analysis and advice for your small business to learn how the Giersch Group's bookkeeping and consulting services can help you overcome issues and grow.

Current Cash Position

To put it simply, for a small business current cash position is the cash in the bank. A more sophisticated view adds cash available from credit lines. However, credit lines are an extension of debt rather than assets and contribute to the need for proper debt management practices. This will not be covered in our discussion on cash flow management.

Anticipating Cash Needs

Anticipating cash needs has two features: near-term and long-term. Small businesses should know whether they have enough cash to get through the year. This should be part of the annual budget cycle covered in November, updated quarterly, and current with the business year. Businesses must be able to anticipate and understand the seasonality of their industry so they can plan ahead. A successful company, through forecasting, must seek to match their cash inflow with their cash needs. Maintaining a Cash Flow Forecast is an essential way to gain understanding about the demands on your company’s cash.

Near-Term Cash Management

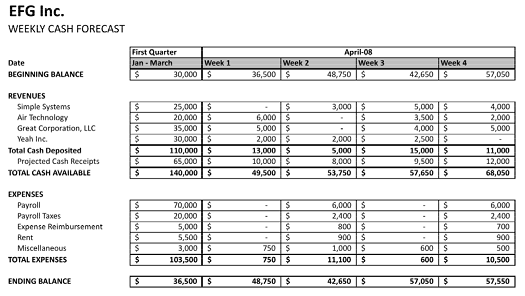

Cash Flow Forecasts (see attachment for example) show how much cash a company receives and the demands on that cash. By tracking the inflow and outflow of cash this forecast provides you with the ability to view your historic and current cash positions. This allows you the opportunity to capture the seasonality of your business and plan accordingly. Cash Flow Forecasts are divided into two parts: revenues (cash in) and expenses (cash out).

- Cash Flow Forecasts start with the balance from the previous period, then add the monies received from clients and subtract the expenses from the current period to show your ending balance.

- The first column contains the total cash in-flows historically, providing you with the ability to forecast future cash flow positions. For example, if rent over the past quarter totaled $5,500, then you know that your monthly rent will be slightly over $1,800 per month. The same is true of payroll and other weekly/monthly expenses.

- Our example shows a weekly method of forecasting cash flow. However, this frequency is not necessary for every company. For example, retail businesses don’t purchase on a weekly basis and recording all the sales and expenses weekly would be extremely time-consuming. Businesses should determine how frequently they should record their cash flow to correspond with the nature of their industry and their overall strategy.

Long-Term Cash Management

Understanding the seasonality of your business is vital to maintaining good cash flow. A company should have a twelve-month cash reserve in order to be considered a going concern. To be able to anticipate and predict the ups and downs of your business cycle it typically takes at least 12 months of tracking your cash position. This is possible only by maintaining and reviewing your Cash Flow Forecast on a regular basis throughout the year. Maintaining a long-term perspective on your company’s cash position will prove important as you choose to save or invest your cash.

Efficiency in Cash Flow

It is necessary not only to match cash inflow with outflow but also to make this flow as efficient as possible. Working capital is a measure of your company’s current assets to current liabilities. A positive number indicates that your revenues are greater than your expenses, while a negative number shows the opposite.

Working Capital = Current Assets - Current Liabilities

However, this measurement is incomplete. There are a number of areas that must be examined when determining the efficiency of a company’s cash flow. The first area is how quickly a company turns sales into cash. Secondly, an evaluation of inventory levels helps to determine how quickly inventory turns into sales. When viewed together these measurements provide a picture of what your company’s cash position looks like, allowing you to make decisions that will affect the efficiency of the cash flow.

Managing cash flow is particularly crucial for service industry businesses. We offer specialized bookkeeping services for companies in many industries, including travel agencies, bars & restaurants, salons & spas, and many more.

Cycle Time

Cycle time deals with the question of how long it takes for a sale to turn into cash. We call the period of time it takes for a sale to go from a receivable to cash a cycle. Days sales outstanding is a measurement of cycle time which describes how long it takes a sale to complete one cycle. For example, if Company EFG receives cash 45 days after the sale, then the days sales outstanding is 45. If this number increases over time then you can deduce that your cash requirements are going up. However, if it decreases you cannot necessarily conclude that your cash requirements are decreasing. The decrease may be contributed to a decline in business, seasonality, or other factors. The goal is to decrease this number as much as possible by reducing the time it takes to receive payment for services rendered. Doing this allows you to free up cash, which can be used to finance your company.

Inventory

Many times businesses only look at how quickly sales turn into cash and completely ignore the other side of the equation–the speed at which inventory turns into cash. The best way to calculate this is by determining a company’s inventory turnover.

Calculate the average inventory:

Beginning Inventory + Ending Inventory ÷ 2 = Average inventory

Calculate the inventory turnover:

Cost of Goods Sold ÷ Average Inventory = Inventory turnover

Calculate the number of days it takes for products to go through the inventory system:

365 ÷ Inventory Turnover = Number of Days to Sell All Inventory

This calculation tells you how many days it takes your company to sell off all its inventory. This number is important because the speed at which the inventory turns into sales has to be commensurate with supplier payment periods. If your days’ inventory is greater, then it requires extra cash. For example, if Company EFG has 30 days’ inventory then the payment terms the suppliers require should also be 30 and the extra cash need will be $0. However, if the company has 60 days’ inventory, but pays its suppliers every 30 days, then the inventory will require 50% more cash to maintain. The goal here is to balance supplier payables with inventory.

Payment Terms for Suppliers

Delaying payment to suppliers until the last day within their terms is an important way to manage cash flow. By delaying payment you maximize the amount of cash in your business, allowing you greater mobility to finance your company. However, many suppliers offer discounts for faster payments. These can be quite valuable to a small business and should not be missed if your cash flow allows. Regardless, it should never be an option to pay suppliers past the negotiated time frame. Paying on time within what is allowed is the most responsible way to manage your cash flow and will not only better your cash position, but also keep relations strong with your suppliers.

Improving Efficiency of Cycle

So what actions can be taken to improve the efficiency of this cycle or bring the speed of the turndown? By engineering these mechanics systematically into your business you will increase efficiency.

- Understand and utilize these ratios:

- Working Capital

- Days Sales Outstanding

- Inventory Turnover

- Increase your speed of billing. Rather than billing once per month, bill customers twice a month. Or issue invoices promptly and follow up immediately. This will increase your cash and allow you to finance your business more efficiently.

- Get Retainers applied to the back end allow progress billings throughout the project and faster cash collection relative to work completed.

- Collecting upon delivery (O.D.) is a great alternative to refusing to do business with someone who pays slowly and is usually past due.

- Offer discounts to customers who pay their bills quickly.

- Utilize electronic fund transfers to make payments on the last day of the payment period.

- Communicate with suppliers. They often hold a great deal of stake in your company and do not want to see you go out of business. Explaining your cash position can help when you need to delay payment. They will often be more interested in keeping your business afloat than a bank would be.

- Pay your bills strategically. Understand seasonality as well as future revenues and expenses through forecasting, then pay your bills accordingly. Make your employees and suppliers priority.

Investment of Funds

What do you do when you have excess cash? The first priority is to understand the seasonality of your business so your investing activities do not cause you to run out of cash. For many small businesses, fees can be as important as interest rates. Free checking and avoidance of fees to a company is often a better investment return than employing your excess cash in interest-bearing accounts that have fees. Just remember, investment is relative to fees. Maintain a minimum cash balance in your company and then put the rest in an account that allows you quick access to your cash and pays only those fees that can justify the investment. Both will be important as a growing company.

Estimated Management Time: 1-hour weekly review

Tutorials & Articles for Further Reading

- “The Art of Cash Management.” This article provides a variety of ways to implement different cash management strategies.

- “How to Better Manage Your Cash Flow.” This article explores many different approaches to improving your cash flow position.

- This website provides a simple Cash Flow Forecasting template similar to the one in the exhibit above.

Contact the Giersch Group online for more information and a free consultation. We have offices in Milwaukee, Brookfield & Madison, WI.